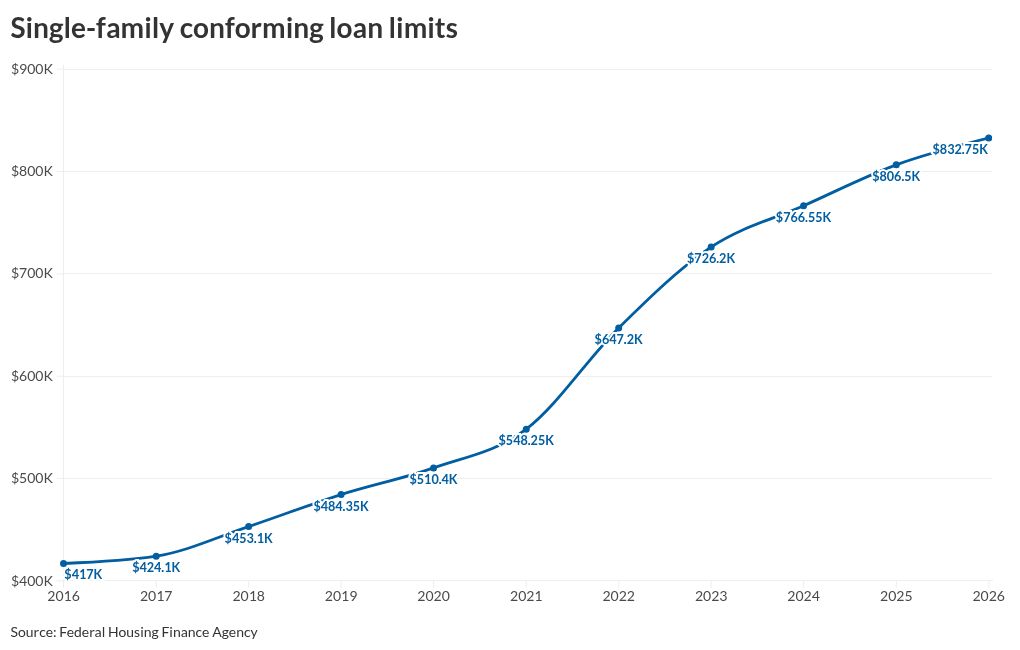

U.S. Federal Housing is boosting the conforming loan limits by 3.26% for 2026 based on the annual change in home prices using an expanded data set.

The new limit of $832,750, is an increase of $26,250 from the 2025 limit of $806,500. The high-cost ceiling for one-unit properties will be $1,249,125, which is 150% of the new limit. This will also be the baseline limit for Alaska, Hawaii, Guam, and the U.S. Virgin Islands.

The Federal Housing Administration will set its program loan limits based on the new conforming amounts.

Earlier in the day, U.S. Federal Housing announced the Federal Housing Finance Agency House Price Index rose 2.2% year-over-year in the third quarter, following a 0.2% gain from the prior three-month period.

The third-quarter index sets the stage for the next year’s conforming loan limits. U.S. Federal Housing builds on that figure with a broader data set that also pulls in numbers from the Federal Housing Administration and Cotality (formerly CoreLogic), according to an agency representative last year.

In the third quarter of 2024, the HPI increase was 4.3%; the expanded data allowed FHFA to raise the limits by 5.2% for the current year. But the expanded data set can also bring the final amount lower. For the third quarter of 2023, the HPI rose 5.5% but the 2024 conforming limit increase was just 5%.

As has become the practice in recent years, several well-known lenders are offering what they call conforming mortgages at next year’s projected limits in advance.

Rocket is accepting loans at $825,500, while United Wholesale Mortgage, Rate, Crosscountry and Pennymac are at $819,000. The Rocket limit is 2.3% above the current conforming loan limits of $806,500.

House prices rose in 44 states and the District of Columbia and in 76 of the 100 largest metropolitan areas over the previous four quarters.

This quarter’s annual increase is the second time under 3% since the second quarter of 2012 when the growth rate was 2.5%, and the lowest since the first quarter of that year, when prices were essentially flat.

The S&P Cotality Case-Shiller U.S. National Home Price Index also was released on Nov. 25, and reported a 1.3% annual gain in September, down from 1.4% for August.

The 10-city composite rose by 2%, down from 2.1% the previous month, while the 20-city composite posted a 1.4% year-over-year gain, down from 1.6%.

“The housing market’s deceleration accelerated in September, with the National Composite posting just a 1.3% annual gain — the weakest performance since mid-2023,” said Nicholas Godec, head of fixed income tradables and commodities at S&P Dow Jones Indices, in a press release. “This marks a continued slide from August’s 1.4% increase and represents a stark contrast to the double-digit gains that characterized the early post-pandemic era.”

Furthermore, the data shows stark geographic differences.

“Markets that were pandemic darlings — particularly in Florida, Arizona, and Texas — are now experiencing outright price declines,” Godec said.

At the same time, Northeast and Midwest states are continuing to post solid value gains, “suggesting a reversion to pre-pandemic patterns where job markets and urban fundamentals drive appreciation rather than migration trends and remote-work dynamics,” Godec continued.

Separately, October’s preliminary annual home price appreciation as measured by the American Enterprise Institute was 1.5%. This was down from 1.7% a month ago, 4.1% for last October 2024 and 5.2% in October 2019.

“October 2025 has the lowest rate of [annual home price appreciation] we have recorded in any month since our series start in 2013, as elevated home prices during the pandemic, higher interest rates since 2022, and a diminishing pool of qualified entry-level buyers are fueling a reversion of pricing to the mean, especially in metros in the South and West,” the press release from the AEI Housing Center said.