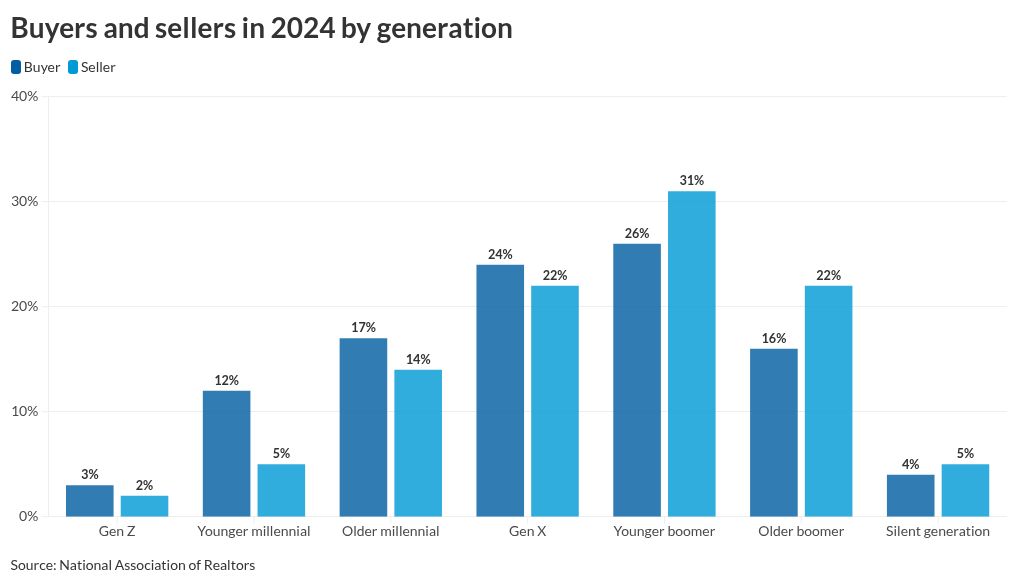

An unexpected generational shift occurred in the home purchase market in 2024, as baby boomers had the largest share of buying activity, while millennials pulled back.

Furthermore, boomers were more likely to pay cash for their new residence, according to the National Association of Realtors’ 2025 Home Buyers and Sellers Generational Trends report.

It is not surprising boomers made up over half of those selling homes. But the data shows that rather than becoming renters, a significant portion are purchasing another property, at 42%; 26% of those are what the report defines as “younger boomers,” those between 60 and 69.

“In a plot twist, baby boomers have overtaken millennials — the largest U.S. population — to become the top generation of home buyers,” said Jessica Lautz, NAR deputy chief economist and vice president of research, in a press release. “What’s striking is that half of older boomers and two out of five younger boomers are purchasing homes entirely with cash, bypassing financing altogether.”

The millennials had a 29% share, down from 38% in NAR’s 2024 study. Gen X, situated between the two groups, was unchanged at 24%.

A Redfin study found homeownership rates flattening among the younger demographics in 2024, with 26.1% of Gen Zers owning their home, compared with 26.3% in 2023 and 26.2% in 2022.

Millennials had similar trends, at 54.9% for last year, versus 54.8% for 2023. Another study, the NextGen Homebuyer Report, found millennials to be more confident about becoming a homeowner than Gen Z.

Small year-to-year increases were seen among Gen X, 72.9% versus 79% and 79.6% compared with 78.8% over the same time frame.

“Some young people are placing less emphasis on owning their own home because they’re prioritizing flexibility, while others continue renting because they can’t afford to buy,” Redfin Chief Economist Daryl Fairweather, said in the report. “Buying a home is still typically a good financial investment, but for young people who don’t have the desire or means to do so, there are other viable investments that, unlike buying a home, don’t require a huge down payment.”

Those under 44 years old were more likely to need to finance their purchase, with 90% doing some form of borrowing, the NAR study found.

Just over one-quarter of the younger millennials, between 26 and 34, had a gift from a relative or friend to help make their down payment. This was true for 13% of the older millennials, those between 35 and 44.

Reflecting the age shift in the overall market, just 24% of recent buyers were first-timers, down from 32% in 2024. Younger millennials (71%) were more likely than their older generational counterparts (36%) to be a first-time buyer.

“Older millennials are buying bigger and newer homes with larger down payments than their younger counterparts,” Lautz said. “This shift reflects the increasing role of equity in enabling repeat purchases, especially among older generations, while younger buyers continue to face affordability challenges.”

Just under half of those between 35 and 44 owned a house prior to their most recent purchase.

The Gen X buyers have the highest median income, at $130,000, followed by the older millennials at $127,500. They are also purchasing homes to accommodate, on one hand, their aging relatives, and on the other side, their children over the age of 18, Lautz said. “While Gen X are purchasing at the highest household incomes, they may still feel the squeeze as they aim to find a home that serves everyone.”

Only 8% of those surveyed who needed financing said the mortgage application and approval process was much more difficult than expected, while 18% said it was somewhat more difficult. But 52% said it was not difficult and 21% found it easier.

A conventional mortgage was the option for 52% of those surveyed, while 29% turned to the Federal Housing Administration program and 9% got a Veterans Affairs loan. Those numbers are similar with Optimal Blue’s February rate lock data.