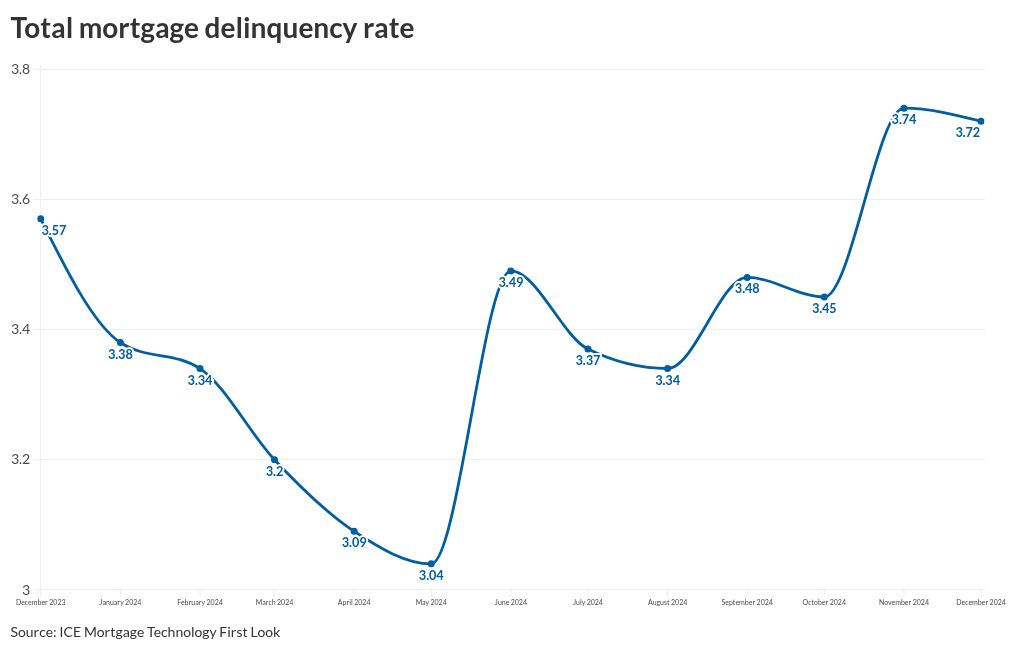

Mortgage performance continues to slip, with the annual delinquency rate rising for the seventh consecutive month, ICE Mortgage Technology’s December First Look report stated.

While the rate is good when compared with normal times (pre-pandemic rates of near 6%), it is still at a three-year high.

The negative trend is likely to continue in the current year.

“We expect mortgage performance to become a growing topic of conversation in 2025, especially among Federal Housing Administration and Veterans Affairs mortgages,” said Andy Walden, Intercontinental Exchange’s head of mortgage and housing research.

Those government-guaranteed mortgage products are the proverbial canary in the coal mine when it comes to delinquency trends, Walden elaborated.

That is because “these products are intended to expand home ownership opportunities for first-time home buyers, and buyers that might not otherwise be able to afford a conventional mortgage with a 20% down payment,” he said. “That has especially been true in recent years as these products have absorbed a larger share of the lower-credit, higher loan-to-value market that had been previously privately securitized.”

December’s rate lock activity found conforming mortgages found their share reduced to 51.2%, down 157 basis points from November and 541 basis points from the prior year, Optimal Blue’s Market Advantage report said. That is the lowest since the product and pricing engine provider started tracking this data in January 2018.

(Optimal Blue had been owned by Black Knight but as a condition of the latter’s merger with Intercontinental Exchange was forced to be divested.)

The FHA share was 21% and VA’s was 11.5%, up 60 basis points and 10 basis points respectively from November. But these were down 53 and 38 basis points versus one year ago.

Nonconforming locks were the big annual gainer, up 635 basis points from December 2023 to 15.7%.

“Notably, conforming loan share has hovered around historic lows for the past five months,” said Brennan O’Connell, director of data solutions at Optimal Blue, in a press release. “This trend illustrates how borrowers are relying increasingly on government and non-conforming loans to finance in a challenging market.”

The total share of mortgages 30 days or more late for their payment, but not yet in foreclosure, was 3.72% in December, ICE said. This was down 20 basis points or 0.6% from November, but up by 15 basis points from December 2023’s 3.57%, an increase of 4.02%.

“Foreclosures remain muted due to the increased prevalence of forbearance and other loss mitigation efforts along with the strong equity footing of mortgage holders in today’s market,” Walden commented.

But the change in foreclosure starts, both from the prior month and year, was still stark.

During December, servicers made 31,000 foreclosure starts, a change of 50.37% compared with November’s 21,000. The increase compared with December 2023 was 29.69%.

At the same time, the foreclosure pre-sale inventory rate of just 35 basis points was up 3.72% from November, yet lower by 10.68% compared with one year earlier.

The total number of properties in delinquency including foreclosure was over 2.2 million, down 4,000 from November but up by 89,000 compared with one year prior.

For properties considered serious delinquent, 90 days or more late but not yet in foreclosure, the numbers increased in December by 29,000 from the prior month and 66,000 over the prior year to 541,000.

The monthly prepayment rate was 57 basis points, 9.83% slower than November but over 47% quicker than 12 months earlier, as mortgage rates were lower compared with December 2023.